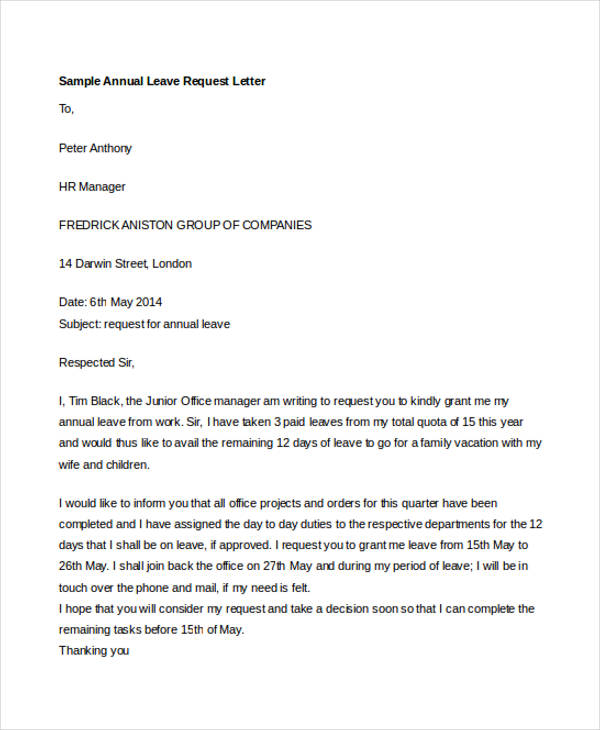

If you find yourself public information in the FHLB improves is relatively sparse, its clear that FHLB players are aware of the aftereffect of FHLBs’ dividends on the total price off borrowing from the bank. As an instance, a page into the FHLB il webpages away from 2019 shows exactly how the bonus paid down so you’re able to interest-mainly based inventory (B1 on photo) consistently exceeds the new dividend paid in order to standard subscription financial support (B2). Moreover it maps how big is the newest active discount into mentioned advance price down seriously to dividends more past quarters; the fresh new dismiss hovers ranging from seven and you can 14 bps:

Another web page reveals the newest Q3-2023 formula, providing good thirteen-bps avoidance to your mentioned progress speed. Furthermore, when you find yourself FHLB Chi town-like most of the FHLBs-doesn’t in public bring historical advance pricing, the homepage does render a regular term layer. And effective progress prices, so it layer provides professionals the newest all-in rate they may be able anticipate paying just after changing with the expected bonus income. The following is a picture away from that sheet (complete file here ) towards the (red-colored markup ours):

New exceptions occurred when FHLB advances turned more pricey versus Given throughout the latter half of 2008 and you may throughout the 2009, and in 2022 and you can 2023-ahead of recently losing below the first borrowing rates once more:

By this new go out of this title layer, the brand new Fed’s dismiss windows try billing 5.5% getting money all the way to 3 months. Meanwhile, the brand new FHLB was charging you a title rate of five.49% to have step 3-times loans, in addition to article-bonus speed shown added members to anticipate a different 13 bps refunded through returns.

FHLB Pittsburgh similarly promotes the benefit of the newest dividend and will be offering professionals which have a presentation of your refund’s influence on the web site. During this creating, the analogy is actually for a-1-12 months get better taken up . They shows that because the stated rate to the get better are 5.72%, asked dividends imply a member can expect so you can efficiently shell out 5.39%-a beneficial 33-bps disregard:

(Notably, yet not, the aforementioned computation divides the interest pricing by full progress quantity of $one million instead of the real exchangeability agreed to brand new debtor, which would getting $0.96 billion. Next modifications, the latest promotion is only eleven bps.)

Within the a document towards the page old , FHLB Atlanta depicts good 21-bps discount into the a 1-seasons improve right down to dividends paid down to help you consumers:

FHLB Des Moines has the benefit of people a dividend write off calculator , and you will a great 2019 speech for members demonstrates a good 19-bps dismiss towards a 1-12 months advance:

Lower than, we area new Fed’s number one borrowing price, the new mentioned FHLB progress pricing having an identical maturity on the write off windows, and all-in FHLB improve pricing one mirror the true price of credit immediately after accounting to have returns repaid so you’re able to individuals. (The precise formula methodology is actually revealed about endnotes. )

When you’re in public areas readily available go out series studies regarding the FHLBs is limited, we can pertain the kind of calculation said of More hints the FHLBs found a lot more than so you can go out collection i obtained from the FHLB De l’ensemble des Moines and you will FHLB Pittsburgh websites

FHLB De l’ensemble des Moines studies, you’ll find back using 2000, shows that brand new all of the-in expense of one’s FHLB improve provides usually started significantly down compared to cost of no. 1 borrowing from the bank.

FHLBank Pittsburgh investigation, limited back as a result of 2020, shows that when you find yourself their mentioned get better price have generally detailed on hook advanced with the Fed’s number one credit rate, the fresh all the-during the borrowing from the bank costs is actually below the pri. The the-when you look at the FHLB cost after that transferred to a notable advanced during 2022 and you may 2023, just before tightening once more has just:

At the start of the fresh pandemic, new Given paid down the fresh pass on billed from the dismiss windows more top of the bound of one’s fed loans finance price (the monetary rules price) so you’re able to no, in which this has stayed. Despite this reduced discount screen cost, which left the new said get better cost of both FHLB Des Moines and FHLB Pittsburgh higher than new Fed’s number one credit rate, the fresh shortly after-promotion cost from the both FHLBs remained lesser compliment of 2020 and 2021. Moreover, its recognized you to definitely one another FHLBs ran off following getting favorable prices to charging a made while in the 2022 and you can 2023-just as need for liquidity was picking right on up. A similar feeling can be seen to possess FHLB Des Moines throughout the the global Financial crisis.

{kind=link}